Mohau Hlonyana asked

Someone who follows him also responded thus, see link to tweet

Mohau Hlonyana, a.k.a Sam's follower's response

I then responded in this manner, see link to tweet

My response to Sam and his follower

To which this person responded as per below, see link to tweet

Response to my response,

and I realised that the person was not convinced.

This discourse inspired this short blog from me. I hope it will teach you something and that perhaps you will leave a comment or question for me to address. Details about my book at the bottom of the page.

Here’s an analogy on living below your means, using the below quoted social grant amounts from 2017

The basis must be historical, because it will be based on factual & not projected performance.

Considering that the Child Grant was R380 as off 1 Oct 17

Calculate 10% 》R380*0.1 = R38

It costs nothing to open a trading account on a trading platform, the below platform is one of the most cost effective

Open a fixed multiple deposit account at a bank, say for 12 months annually

Take R20 to the Fixed Deposit Account, capitec-bank-1-year-fixed-term-deposit rate, you can calculate what interest the R20 deposits into the FDA would have yielded over the period under consideration if you fixed it with Capitec.

Then take the R18 to Tax Free Savings Account on EE

In the Tax Free Savings Account, say you buy Preftrax ETF (I chose this Exchange Traded Fund for my example because it costs less than R10 and I have owned it so I have the factual yield data to reference. End of 2017 it had a dividend yield of 9.89% for the cost price of R8.82 per share to me)

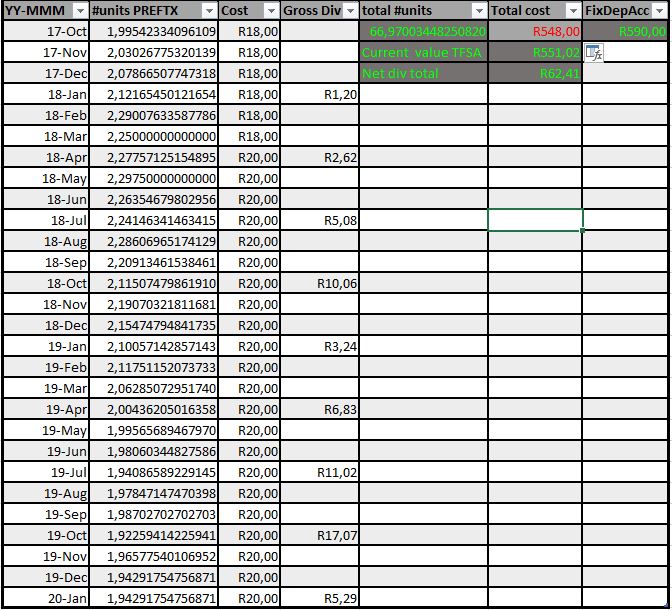

So you bought, for R18, 1. 995423340961098 units of PREFTX at the investment value of R17.44 + cost

of R0.56 on Oct 2, see image example of price below as found on PREFTX price movements graph

Did the same in November, put away R20 in FDA and bought 2.030267753201397 of the ETF

Repeated in December, put away R20 in FDA and bought 2.078665077473182 of the ETF

Also in January 2018, put away R20 in FDA and bought 2.121654501216545 of the ETF

You now have 8,22601067285220 units of the ETF in the TFSA and R80 plus interest in the FDA

By

January 22 2018 you receive gross dividend of R0.1464

This come to R1.20, which is arrived at by R0.1464 * 8,22601067285220, that is not taxed.

You stay the course by buying every month and depositing as per above.

In the image below, is a summary of the above strategy, if it had been diligently implemented in the TFSA, which attracts no Dividend Withholding Tax, so all gains are not taxed.

At the end of 28 months (October 2017 to January 2020) this is what that sacrifice would have achieved. (Green is your gains and red your spend)

Since the grant gets increased twice a year, below is the year-on-year breakdown

2018 1 Apr R400 * 0.1 = R40

R20 TFSA, R20-R21 FDA

2018 1 Oct R410 * 0.1 = R41

R20 TFSA, R21 FDA

2019 1 Apr R420 * 0.1 = R42

R20 TFSA, R22 FDA

2019 1 Oct R430 * 0.1 = R43

R20 TFSA, 23 FDA

The below image shows the strategy with increased contributions in line with grant increases.

If you have read up to this point, it means you are truly interested in your #FinancialHealth and are pursuing #FinancialHealth2020 and beyond challenges.

Visit this link to buy my book, titled #Senyethe on Smashwords or Amazon, which tells of my journey into investments and how I formulated the strategy I implemented on my portfolio. You can read a sample, if you like what the sample shares, you can buy the book

Below is the the portfolio's 2019 performance

First half dividends after DWT R7989

Second half dividends after DWT R6226.43

Good day.